While the Approved Retirement Fund (ARF) distribution is compulsory, some clients who are in receipt of other income choose to invest the after tax ARF income to access it at a future date. We have been looking at tax efficient investment options for these clients and one option is the Employment and Investment Incentive Scheme (EIIS).

The Opportunity

The EIIS is a tax relief incentive scheme, which enables investors to deduct a portion of the cost of their qualifying investment from their total income for income tax purposes for investment in qualifying small to medium sized companies. EIIS is one of the few remaining sources of total income relief. The maximum investment allowed is €250,000 per year.

How does the tax relief work?

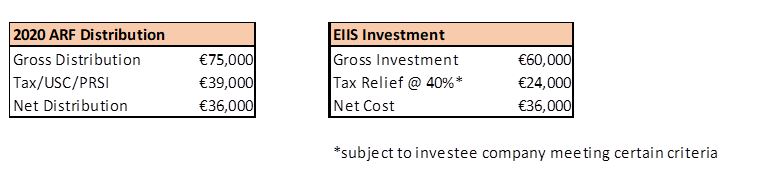

John has an annual distribution from his ARF of €75,000. His other income funds his lifestyle and he is concerned that he has a significant tax liability on his ARF distribution.

As a result he chooses to invest €60,000 in one or more EIIS investments in 2020. The cash flows and tax relief would then work as follows;

John’s investment return in Year 4 would be €60,000 plus/minus the investment return. The investor return is subject to Capital Gains Tax.

As we are not EIIS product producers, Harvest Financial Services Limited is uniquely placed to research the market to recommend the most appropriate investment opportunities for our clients and we currently have a number of interesting EIIS investments opportunities available.

Please note that EIIS investment is a private equity investment and is considered a high risk investment. Your client manager will discuss the appropriateness of this investment with you before any investment is made.

To find out more about these EIIS investments please contact us on 01 2375500 or email justask@harvestfinancial.ie.