Market Insights April 2024

Current Topics in Markets

Surprisingly strong economic data from the US in recent days has caused financial markets to become a little unsettled. The US swaps market is now indicating that total interest rate reductions in the US will be less than 1% this year. We had flagged this in our previous bulletin when we suggested that market optimism around interest rate reductions was on the high side. On the other hand the stronger economy will provide a tailwind to US equity markets so its certainly not all bad news. Attention has now switched to the ECB as the most likely of the major central banks to reduce rates. It has, however, been beaten to the post by the Swiss Central Bank who have already commenced rate reductions.

The European economy is also presenting an interesting picture. While Germany is struggling somewhat, Italy and Spain, more commonly the economic laggards of Europe, appear to be doing quite well. A combination of falling interest rates, some European economic bright spots and attractive valuation levels compared to the US have helped to refocus attention on European markets. Interest rates diverging may also lead to relative dollar strength and we may be looking at the prospect of euro/dollar parity over the course of 2024.

Other themes we are currently watching and which will have an impact on investor returns in the current year include:

Geopolitics – notably the US election and relations between the US and China

ESG – there has been clear evidence of ESG fatigue amongst investors in recent times which has had an impact on ESG focused stocks and funds

Valuations – the valuation gap between US large cap stocks and other stocks (including US small caps, European equities and emerging market equities) is wider than it has ever been and this presents both risks and opportunities.

Equity Markets

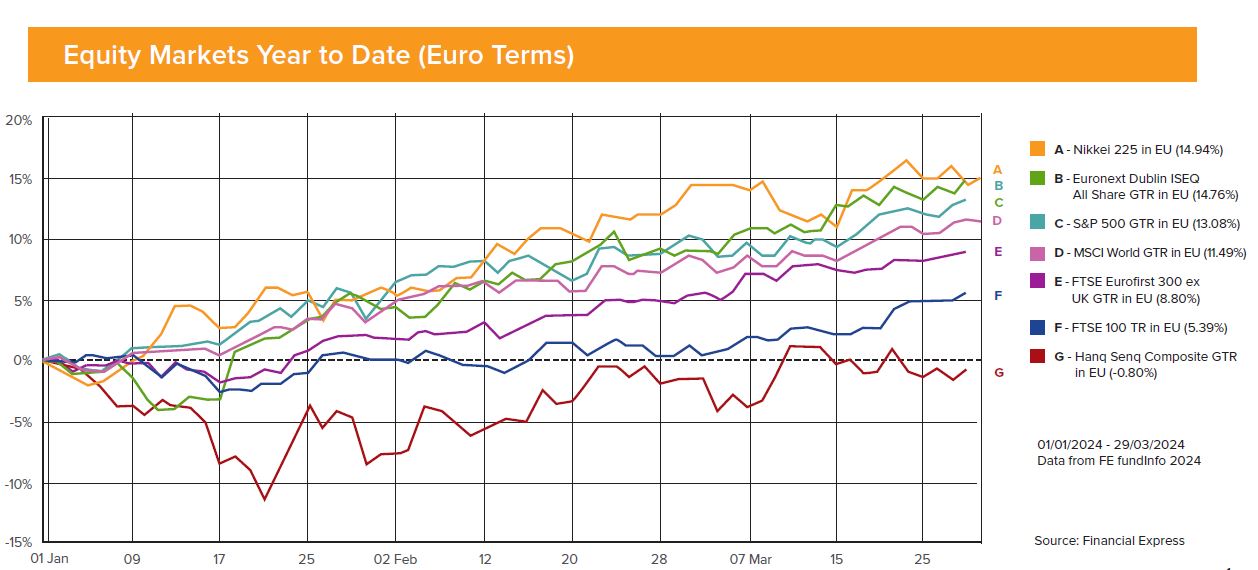

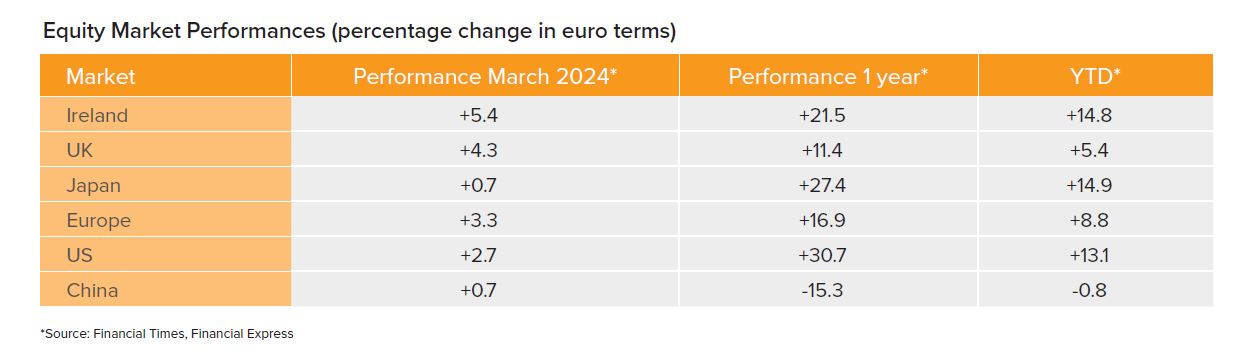

The first quarter has been a strong period for equity markets across the board driven by the optimism around an economic soft landing and the likelihood of interest rates falling. With rate reductions being pushed out and large company valuations looking stretched, this optimism has waned in recent weeks and markets look to have plateaued for now. This is particularly the case in the US and further market progress is most likely going to need an improving corporate earnings outlook and for earnings disappointments amongst the majors to be kept to a minimum.

Away from the US, the value opportunity in both Europe and emerging markets looks very convincing. Despite the mixed economic picture, European equities look cheap and offer an attractive medium term investment prospect. Emerging market equities also look to offer value although a strong dollar and an uncertain economic picture in China could weigh on many of these markets for some time yet. On balance however, we are encouraging investors to focus on quality and value when it comes to selecting equity investment fund options.

Bonds

In contrast to equity markets, the investment case for bonds looks much more clearcut. Quality bonds, both sovereign and corporate, are mostly trading at material discounts to their par values and are offering yields as high as 6% to investors. While the timing of interest rate reductions is uncertain, the trend is clear. As interest rates fall over the next two years, the prices of these bonds will move back towards par, generating a capital uplift for bondholders. While waiting for this gain to materialise, holders can meanwhile enjoy the very attractive yields being paid out.

Property

Property as an asset class fell hugely out of favour during and after covid. While this change in sentiment was justified in the case of retail and office properties, the switch in sentiment has been indiscriminate and affected all sectors of the market. To a significant extent this was because of the sector’s vulnerability to higher interest rates given that borrowing is commonly used to purchase property. However, funds with low levels of leverage and exposed to strong sub-sectors such as logistics, healthcare and even residential have all suffered and currently represent a very attractive medium term buying opportunity for patient investors.

Alternatives

Alternatives is something of a catch all asset category and includes a various mix of asset types including hedge funds, infrastructure funds, renewable energy etc. Because their returns are seen to be income based many of these asset categories have underperformed in recent times. Renewable energy has doubly suffered because of the general malaise overhanging ESG related investments. However, in our view this has been very much overdone and we are encouraging clients to take advantage of the strong combination of value and high income currently being offered.

Our Fund in Focus for April 2024 is – Polar Capital Technology Trust

As always, you should only consider the investment views contained in this April Market Insights update in the context of your own attitude to risk and how such choices might impact your Asset Allocation model. Should you wish to discuss your investment portfolio, please contact Harvest Financial Services on 01 2375500 or email justask@harvestfinancial.ie.